How Call Options Move Relative to Stock Price and Time

In this blog post, we’ll examine buying call options that are 2% out of the money and how its stock price will impact Delta, Gamma, Theta, and Vega. We’ll study 30, 45, 60, and 90 days till expiration as the time intervals.

First some education….

1. How Call Options Move Relative to Stock Price: Delta & Gamma

Delta: Measures how much the call option price moves for a $1 increase in the stock price.

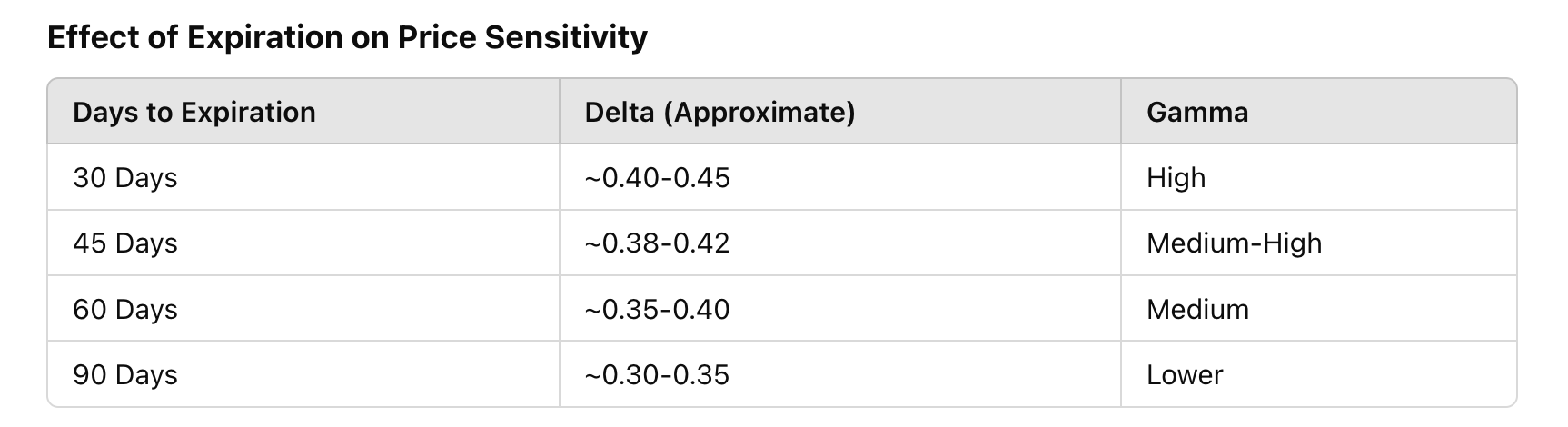

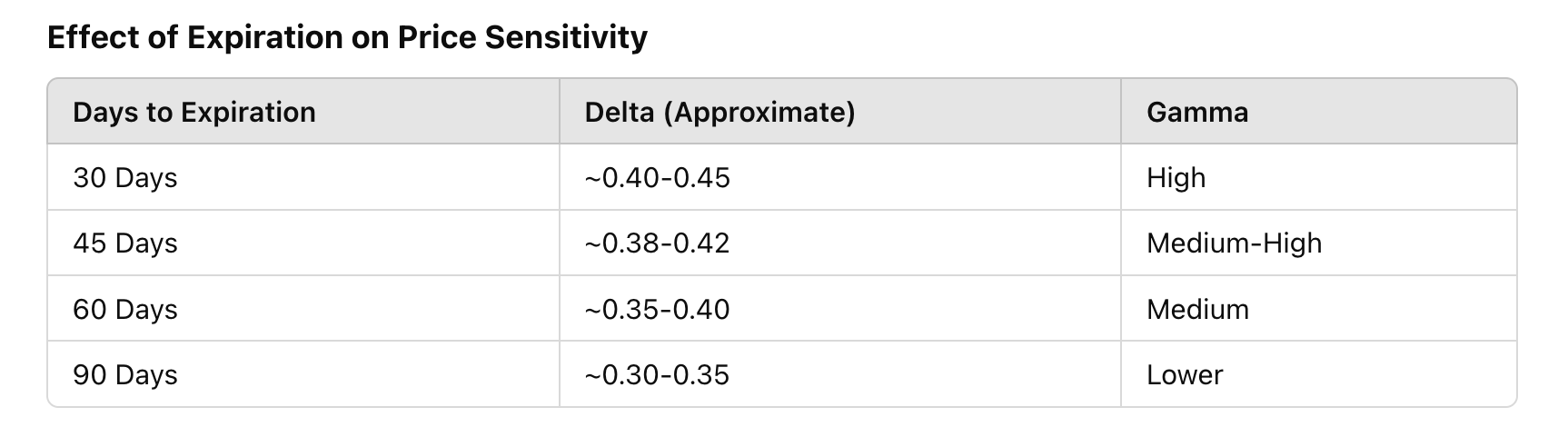

Since these calls are OTM (2%), their delta is between 0.30 and 0.45 (closer to 0.30 for longer expirations and closer to 0.45 for shorter ones).

As the stock price increases and approaches the strike price, delta increases, moving toward 0.50–0.60 (at-the-money) and then closer to 1.00 if deep in-the-money.

A shorter-term option will have a higher delta for the same moneyness than a longer-term option.

Gamma: Measures how much delta changes for a $1 move in the stock price.

Gamma is highest for options that are near expiration and near the money.

Shorter expirations (30 days) have higher gamma, meaning the option price responds more dramatically to stock price movements.

Longer expirations (90 days) have lower gamma, meaning delta changes more slowly.

Effect of Expiration on Price Sensitivity

Shorter-term options move more sharply as price nears the strike price because gamma is higher.

Longer-term options move more steadily but have more muted reactions.

2. How Time Decay Affects the Call Option: Theta

Theta: Measures how much value the option loses per day due to time decay.

OTM calls lose value fastest closer to expiration.

Theta increases as expiration approaches (accelerates in the last 30 days).

Longer-term options lose value more slowly.

Effect of Expiration on Theta (Daily Time Decay)

Takeaway: If you buy a 30-day call, time decay will be much more aggressive than a 90-day call.

3. How Volatility Impacts the Call Option: Vega

Vega: Measures sensitivity to implied volatility (IV).

Longer-term options have higher vega, meaning they gain or lose more value when IV changes.

Shorter-term options have lower vega, so IV changes impact them less.

Effect of Expiration on Vega

Takeaway:

If you expect a volatility increase, longer-dated calls (90 days) benefit more.

If IV collapses (e.g., after earnings), longer-term options lose more value due to high vega.

4. Summary: Choosing Expiration for a 2% OTM Call

ExpirationProsCons30 DaysHigher gamma (sharp moves up when ITM), cheaper premiumFast theta decay, sensitive to short-term movements45 DaysGood balance between movement and decayStill loses value quickly if stock doesn’t move60 DaysMore time to be right, lower decay than 45-day optionsSlower price response than 30-45 days90 DaysLeast time decay, benefits from volatilityMore expensive, moves slower due to low gamma

5. Practical Considerations for Trading These Calls

If you expect a short-term breakout, buy 30-45 DTE calls (higher gamma, faster movement).

If you want more time and lower decay, buy 60-90 DTE calls (safer but slower-moving).

If implied volatility is low and you expect it to rise, longer-dated calls are better.

If IV is high (e.g., before earnings), avoid long-dated calls due to high vega risk.

Rolling 30-45 day calls before theta decay accelerates (within 10-15 days to expiration) can help mitigate time decay losses.

Example analysis with Amazon (220 Strike Calls with April 17th, 2025 Expiry): 50-53 Days til Expiry

1. Current Stock and Option Details

Current AMZN Stock Price: $214.85

Strike Price: $220

Days to Expiration: Approximately 53 days (from February 24, 2025, to April 17, 2025)

Since the current stock price ($214.85) is below the strike price ($220), this call option is out-of-the-money (OTM) by about 2.4%.

2. Option Pricing and Greeks

As of February 21, 2025, the option chain data indicates:

Bid Price: $6.95

Ask Price: $7.15

Implied Volatility (IV): 27%

The mid-point price (estimated fair value) is approximately $7.05.

Greeks (approximations based on typical OTM options with similar parameters):

Delta: ~0.40

Gamma: ~0.02

Theta: ~ -0.04 per day

Vega: ~0.10

3. Price Movement Relative to Stock Price

Delta (~0.40): For every $1 increase in AMZN's stock price, the option's price is expected to increase by approximately $0.40.

Gamma (~0.02): Indicates that for every $1 move in the stock price, Delta will change by 0.02. If AMZN rises by $1, Delta would increase to 0.42, making the option more sensitive to further price changes.

Example: If AMZN's stock price rises from $214.85 to $220:

Initial Delta: 0.40

Price Increase: $5.15

Estimated Option Price Increase: 0.40 * $5.15 = $2.06

New Option Price: $7.05 (initial) + $2.06 = $9.11

As the stock approaches the strike price, Delta increases, leading to larger changes in the option's price for subsequent stock movements.

4. Time Decay Impact

Theta (~ -0.04 per day): The option loses approximately $0.04 in value each day due to time decay.

With 53 days until expiration, the total time decay impact would be:

Total Theta Decay: 53 days * $0.04/day = $2.12

This means that, all else being equal, the option's price would decrease by $2.12 over the next 53 days due to time decay alone.

5. Volatility Impact

Vega (~0.10): For each 1% change in implied volatility, the option's price changes by $0.10.

If implied volatility increases from 27% to 30% (a 3% increase):

Price Increase: 0.10 * 3 = $0.30

Thus, the option's price would increase by $0.30 if implied volatility rises by 3%.

6. Summary

Stock Price Movement: A $1 increase in AMZN's stock price increases the option's price by approximately $0.40.

Time Decay: The option loses about $0.04 in value daily due to time decay, totaling $2.12 over the next 53 days.

Volatility Changes: A 1% increase in implied volatility adds approximately $0.10 to the option's price.

Understanding these dynamics helps in anticipating how the option's price may change with movements in the underlying stock, passage of time, and shifts in volatility.

Note: Option prices and Greeks are dynamic and can change with market conditions. The provided values are approximations.

Well, how do we measure Implied Volatility for an individual stock? Here’s an example:

Changes in implied volatility (IV) are not directly measured by the VIX, but the VIX can provide a general market-level reference for volatility trends. Here's how you can track changes in IV for specific stocks and options:

1. VIX vs. Implied Volatility (IV)

VIX (CBOE Volatility Index): Measures the expected 30-day volatility of the S&P 500 index based on options pricing.

It’s a broad market volatility gauge, not specific to individual stocks.

If the VIX is rising, it suggests increasing market uncertainty, which can increase IV for many stocks.

If the VIX is falling, it suggests decreasing fear, leading to lower IV across stocks.

Implied Volatility (IV) of Individual Stocks (e.g., AMZN):

Each stock has its own implied volatility, which fluctuates based on demand for its options.

AMZN’s IV is affected by company-specific events (earnings, news, macro trends) rather than just the VIX.

2. How to Measure Changes in IV for AMZN Options

Option Chain Data: Most brokers (e.g., TD Ameritrade, Interactive Brokers, ThinkOrSwim, TradingView) display IV for each option contract.

IV Rank & IV Percentile:

IV Rank: Compares current IV to its past 52-week range (0 to 100). A high IV Rank (e.g., 80+) means IV is near yearly highs.

IV Percentile: Shows the percentage of time IV was lower than the current level over the past year.

3. How IV Changes Affect Call Options

If IV Increases: Option prices rise (good for call buyers, bad for sellers).

If IV Decreases: Option prices fall (bad for call buyers, good for sellers).

4. Practical Example (AMZN 220 Call, April 17 Expiry)

Current IV: 27%

If IV rises to 30%, the option price increases based on Vega.

If IV drops to 24%, the option price decreases.